Australia | Feb 05 2008

By Greg Peel

Dr Steve Keen, Associate Professor of Economics at the University of Western Sydney, has long advocated that Australia is facing a spiralling debt problem that dwarfs inflation as the primary economic concern. The global credit crisis has done nothing to undermine Dr Keen’s resolve.

Like most others, Dr Keen believes the RBA will raise the cash rate to 7.00% later today. But he sees it as the wrong move.

The RBA is determined to fight Australia’s growing inflation problem – a problem which cannot be denied. The Fed is currently choosing to play down inflation concerns, while addressing the US debt problem which has seen housing prices collapse and mortgages default. While clearly the US has a much bigger problem than Australia at present, even allowing for per capita adjustment, the divergence between the two central bank policies has become extreme.

“Australia’s ‘Rambo’ RBA is still waging the war against inflation, while the ‘Sensitive New Age’ Federal Reserve is clearly trying to soothe the financial markets,” says Dr Keen, in his latest Debtwatch report. In mid-2006 the differential between US and Australian rates was 0.5%, and now it is 3.75% (4.00% if the RBA rises today). The last time there was such a policy disconnect was in the period 2002-06. But in that case the bursting tech bubble had a much more profound effect in the US than was ever felt in Australia.

Over that period, the US growth rate fell to 0.2% while Australia’s remained above 1.5%. Dr Keen believes the RBA is banking on the recent bubble – the credit crisis – once again being contained within the US. But what if, in fact, this bubble proves to more replicate the previous period of disconnect, in the 1990s?

In the 1990s, both countries experienced a stock market bubble and crash followed quickly by a commercial property market bubble and crash. Australia increased interest rates far more aggressively than the US in order to rein in both inflation and the property market. It worked – inflation was tamed. But the other result was a fall in Australia’s growth rate from 2% above the US to 3% below it. The resultant recession in Australia was deeper and longer than that in the US. Over the next three years, Australia had to drop rates rapidly from 18% to 5%.

That the Fed is now lowering rates and the RBA raising them suggests both cannot be right, unless the two economies are simply that much different, Dr Keen offers.

“The difference in rates of economic growth are exaggerated by the US practice of multiplying the current quarter’s rate of growth by four to estimate the annual rate of growth; Australia, on the other hand, uses the rolling sum of the last 4 quarters to estimate the annual rate of growth. When the less volatile Australian standard is applied to both economies, Australia’s economy still appears to be growing more rapidly than the USA, but the current gap is just one percent.”

At the same time, the current Australian and US CPI inflation rates are almost identical, and well below the mean for the last two decades. So with economic growth much the same, and inflation the same, any difference would have to come down to asset markets. The problem in the US is obvious – falling house prices which have precipitated the credit crunch – but the RBA clearly feels (and has said as such) that there is little equivalent problem in Australia beyond a small section (mostly western Sydney), and that the real problem is growing inflation brought about in a growing economy.

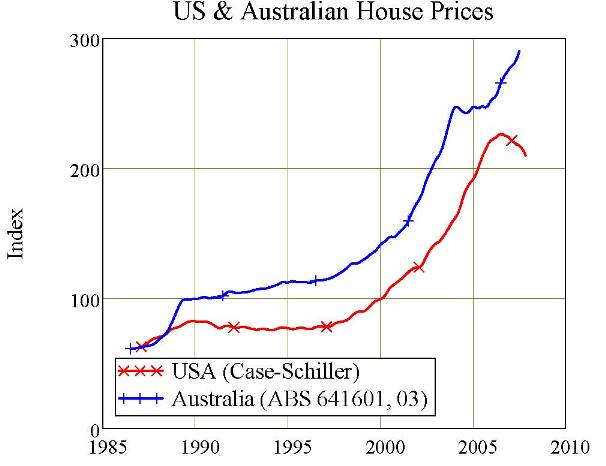

“I think the RBA’s judgment here is flawed,” says Dr Keen. “On the data, the Australian stock market has outdone the US market on irrational exuberance since mid-2004, while the Australian housing market makes the US look subdued by comparison. The historic parallels are not with 2000, but with 1987/89.”

Since mid-2004, the Australian stock market has been in a bubble, averaging 20% growth compared to a 9% average over the previous two decades. The US growth rate has been 13% compared to the equivalent average of 11%. Both countries have experience bubble economies with similar reflections in their stock markets, Dr Keen suggests. But the big difference is in housing.

Our bubble, suggests Dr Keen, makes the US bubble (now burst) look “positively anaemic”

.”Ours began earlier, climbed higher, grew faster, and is still growing – whereas the US’s market is clearly in free-fall.”

Both have or had been driven on the misconception that housing prices can forever rise faster than consumer prices, such that leveraged housing speculation is a guaranteed “road to riches”. But once such a bubble bursts, as all bubbles eventually do, all one is left with is overvalued assets, much higher debt, and a compromised financial sector. This is exactly what’s happened in the US.

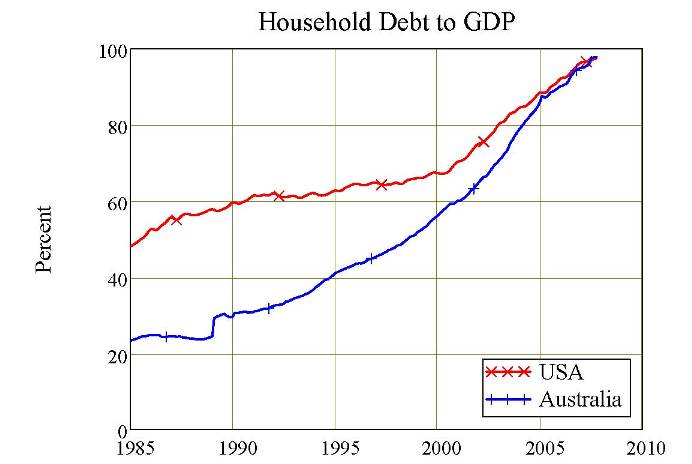

Are Australian houses overvalued? Well across the developed world house prices are currently falling, except in Australia, despite Australia raising interest rates. A recent JP Morgan report suggests another RBA rate rise could put 750,000 mortgage holders under threat of delinquency, and 300,000 of those under threat of default. And while Australia did not fall into the real subprime mess, including the infamous problem of Adjustable Rate Mortgages, the truth is Australia’s household debt to GDP ratio was only half of that of the US in 1985, but is now the same.

Dr Keen notes that but for a few casualties such as the Centros and Allcos, Australia has not suffered to the great extent the US has in the credit crunch. Mortgage default and personal bankruptcy rates are much lower. On the mortgage front, one reason is that in the US a mortgagor can simply hand over the key to the house as satisfaction of the mortgage, leaving the mortgagee to sell the property at a big discount. In Australia the process is more cumbersome, Dr Keen notes, as lenders mostly pressure the homeowner to sell the house themselves to satisfy the mortgage. A mortgagor sale does not result in such a steep discount on sale that a mortgagee sale does.

All this leads Dr Keen to believe that Australia is not immune, and is not particularly different to the US. The only real difference is the “China effect”, which does provide Australia with some quarantine from the problems in the US, he concedes.

“But if irresponsible lending, rising household debt, and unaffordable house prices have caused a financial crisis in the USA, then sooner or later, we’re in for a bigger one still here.”

In which case the RBA is only adding to the problem, in Dr Keen’s view.