Australia | Mar 05 2009

By Andrew Nelson

The Reserve bank’s decision not to cut the interest rate this month was a surprise on an official basis, given the market consensus was for a cut of 25-50bp. However, there were few that were actually surprised, with more and more economists and market watchers predicting the possibility of a pause in the days leading up to the decision.

The RBA was at pains to point out the size of the policy stimulus, both fiscal and monetary, now flowing through the Australian economy. And that the monetary policy transmission mechanism was working more effectively in Australia than elsewhere, and that the Australian financial system remains strong. The central bank warned however, that despite these positives, “economic conditions are clearly weak, and given the speed and scale of the global economic deterioration and its effect on confidence, weak conditions are likely to continue in the near term”.

The bulk of the analysts and economists monitored by FNArena agree that the onset of the recession (or near recession, depending who you talk to) will see GDP growth continue to slacken (just look at yesterday’s read) and unemployment continue to rise. This will ultimately put a cap on inflation, meaning the preponderance of opinion predicts more rate cuts will be needed to steady the ship and slow the overall economic decline. In fact, the RBA remains so relaxed about prices that it devoted few words to inflation, noting, “inflation is likely to decline over time”.

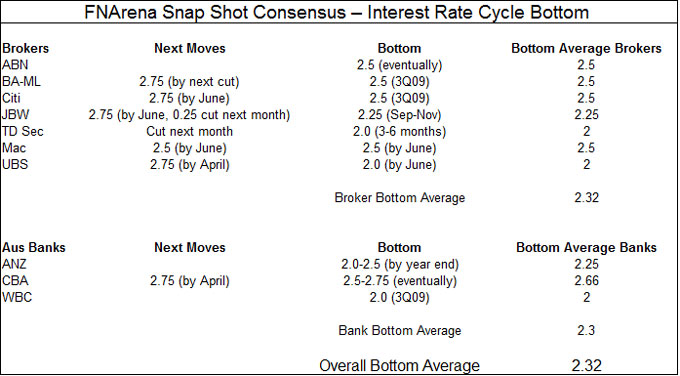

The only significant differences in opinion within the Australian broking and banking communities are: When will the next cuts take place? What will the ultimate bottom be? And when will we hit that bottom? And even these assessments are fairly consistent across the banks and brokers tracked by FNArena.

That said, there is a slight divergence between the outlook from the brokers and the outlook from the banks in regard to timing, if not the ultimate resting place. The data show that the brokers are more readily calling for the cutting to resume sooner. Most brokers tracked expect a cut to at least 2.75% by the June RBA session. Only one of the three banks we polled holds this opinion, while the other two make no short-term calls and push out their bottom predictions to three to ten months down the track.

As far as the ultimate bottom goes, we find the brokers sitting a little higher than the banks, with the former at 2.32% versus the latter at 2.3%. But again, this is the only real difference between the two groups. While there are a few brokers, such as Macquarie and UBS, calling for a bottom of 2-2.5% by June, most of the others are pushing the bottom out until some time in the third quarter, or later. It’s an interesting note that the majority of those expecting the bottom to come further out in the year also have 2.5% as their final target.

There are a few exceptions. The first is TD Securities, who is expecting a rate cut next month much like UBS, and who also expects the bottom of the cycle to be 2%, the same as UBS. The difference between the two is that TD expects the rate to hit 2% some time in the third quarter, while UBS still holds for 2% by June. As of this morning, GS JBWere is also predicting a 0.25% cut next month and another the month after, binging the rate to 2.75% by June. But the stockbroker’s base of 2.25% doesn’t happen until around the end of 3Q to the beginning of Q4.

Macquarie is of the opinion that it just isn’t good enough for a central bank to say that because its official interest rates are already low, it has done enough to support the economy. This is the mistake the European Central Bank has consistently made, with the result being Europe’s economy is much weaker now than it really should be. This leads the broker to think that policy will eventually have to be loosened even more aggressively due to the weakening state of the Australian economy.

Only one bank has gone on the record as far as a next move goes, and that’s Commonwealth Bank. CBA’s economists are calling for a move to 2.75% by next month. However, that’s where their aggression stops, with the bank expecting that the move to 2.75% could indeed be the bottom, while leaving the door open for one more 25bp reduction at some time in the not too distant future. In fact, Commonwealth Bank Senior Economist John Peters says it almost looks like it is time to be talking about when the official cash rate will turn up again. However, with inflation heading for the bottom of the target zone and unemployment rising, he thinks the best forecast for the time being still looks to be for the cash rate to remain at the low point for an extended period.

The other two banks are predicting a bottom at 2.0% and 2.5%-2.75%, but neither expect it to be achieved until some time in the third quarter to the end of the year.

Now it’s important to point out that these were the numbers and predictions pre yesterday’s GDP release, but what’s even more interesting is that the views and forecasts, as yet, haven’t changed that much. In fact, CommSec chief economist Craig James notes that given the weakness elsewhere, the GDP data were not a great shock and he continues to view the data as evidence of a slowdown for the economy and not an indicator of an impending recession. This means the worse than expected GDP result has as yet had no impact on CommSec’s interest rate outlook.

One exception to this lack of rate forecast reaction is GSJB Were, whose economists have moved from thinking there will be no cuts until at least September, to now think there will be two 0.25% cuts in a row, bringing the rate down to 2.75% by June. They still expect another 0.5% worth of easing in September to November, bringing their final bottom estimate down to 2.25% from 2.5% yesterday.

The broker says the 0.5% contraction in GDP was an “unequivocally weak” result and indicates the RBA’s more upbeat outlook is way off the mark. GSJBW labels claims that Australia might be avoiding recession as “strange”. The broker expects another 0.3% contraction in GDP over the March quarter, which it says would open a big gap between what the RBA endorsed as its base-line view just a few days ago and what now appears likely.

Conversely, ANZ Banking Group head of Australian economics, Warren Hogan, believes while the GDP result means the RBA will certainly need to lower its growth expectations for the economy, he still doesn’t see the outcome as forcing the RBA to change its current course. This implies further rates cuts in coming months, as already forecast, but the easings in his view, will be gradual.

In between the two sits TD Securities’ senior strategist Joshua Williamson, who suggests the worse than hoped for GDP data will almost certainly result in additional fiscal stimulus measures, likely accompanying the Federal Budget in May. He notes it also supports his view the RBA will begin to lower rates again from next month. He still expects, however, that interest rates will trough at 2.0% (or possibly lower), but not until some later point in the year.