Australia | May 27 2009

By Rudi Filapek-Vandyck

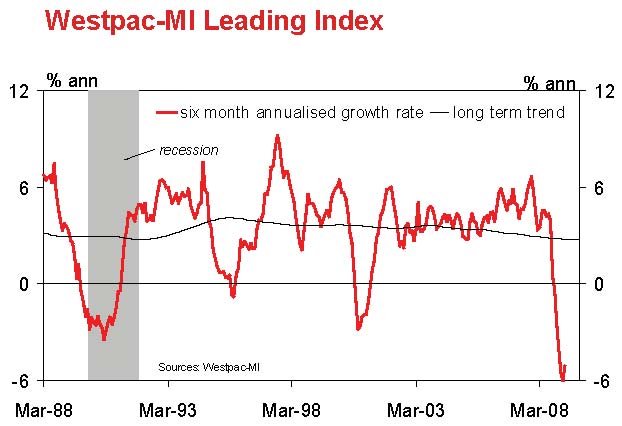

The annualised growth rate of the Westpac-Melbourne Institute Leading Index, which indicates the likely pace of economic activity three to nine months into the future, recorded a negative -5.1% in March, well below its long term trend of 2.8%, Westpac economists report. The annualised growth rate of Coincident Index was 0.7%; also well below its long term trend of 3.3%.

The economists report that, while the Index continues to point to recessionary conditions in Australia, there nevertheless has been a slight improvement in March. The annualised growth rate rose from a negative -6.0% in February to a negative -5.1% in March. The economists point out as such March represents the first substantive rise since April last year. That said, clearly the Index is coming from an extremely weak starting point; the February read was the weakest read the economists have seen in the Index since August 1982.

The March reading is a little bit better (from the historical low recorded in February).

The slight improvement in the Index is consistent with indicators suggesting the pace of contraction in the global economy has eased in recent months.

However, the economists are quickly to add, any recovery still looks to be a long way off. The March reading for the Index remains deep in recession territory, implying a likely further contraction in activity through the middle of 2009.

Explain the economists: even if the Index would record similar improvements in the months ahead it will take three or even four months for the Index to return to levels consistent with positive growth. Westpac suggests this implies a recovery in the real economy is unlikely before the December quarter – at the earliest.

In spite of the improvement in March, the annualised growth rate of the Leading Index has still fallen sharply over the last five months, from minus -0.4% in October to a negative -5.1% in March. The major components driving the 4.7ppt drop have been: commodity prices (-2.5ppts); US industrial production (-2.0ppts); overtime worked (-0.4ppts); productivity (-0.4 ppts); and corporate profits (-0.2ppts). There were positive contributions from shares (+0.6ppts) and dwelling approvals (+0.2ppts).

The level of the Leading Index rose by 0.7 points (+0.3%) in March. Two of the four monthly components rose in March. The all ordinaries index rose 7.1%, marking the index’s strongest monthly gain since June 2000 as well as the first positive result since August last year. Equities have risen a further 5.8% since March, the economists point out.

Dwelling approvals also rose in March, climbing 3.5%. Against this, US industrial production recorded another hefty 1.5% fall in March while the real money supply was down 0.1%. The level of the Coincident Index rose by 0.2 points (0.1%). A strong 2% rebound in real retail trade more than offset negatives from a 0.3% fall in employment and further rise in the unemployment rate from 5.2% to 5.7% in March, reports Westpac.

The weakening labour market has been the main contributor to the slowdown in the annualised growth rate from 1.8% in October to 0.7% in March. A surprise bounce in jobs will see this negative contributor ease in April though the labour market is expected to see a renewed deterioration over the rest of 2009, the economists note.

Notably, they point out, the growth rate in the Coincident Index has remained positive overall. This contrasts with previous recessions that have seen substantial contractions in the Coincident Index.

The Reserve Bank Board next meets on June 2. Westpac expects the RBA to again hold rates steady. A little further down the track, contracting economic activity, deteriorating labour market conditions and a more constrained fiscal policy position are still expected to prompt further easing.

Westpac anticipates the RBA will resume cutting official interest rates in August with a further 1% reduction in the cash rate by the end of 2009.