Australia | Feb 02 2010

By Rudi Filapek-Vandyck

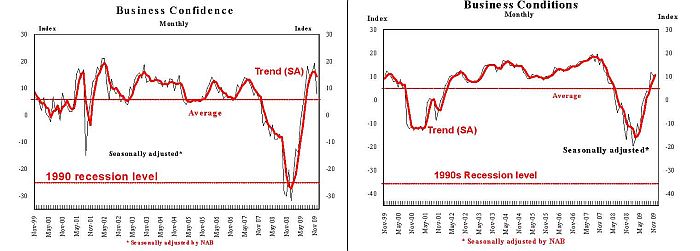

National Australia Bank’s monthly survey into business conditions and confidence has -surprisingly- revealed a large drop in overall business confidence, leading NAB economists to point out that confidence remains above long run average levels.

There was better news on the business conditions side of the survey as they remained unchanged at high levels. Further, trading, profits and employment all marginally improved, with labour market improvements more pronounced. Forward orders and stocks were broadly unchanged and capacity utilisation moved higher again, reflecting strong growth momentum.

Wage and price pressures are still low, but both have increased in recent months. Say the economists: especially wages. Purchase costs also remain low but are building. Retail prices remained flat in the month. This, say the economists, is reflecting weaker sales.

National Australia Bank has lifted its global growth forecasts to a negative 1.1% in 2009 and a positive 3.50% in 2010 (from 3% previously). The upgrade fundamentally reflects stronger growth in China and Non Japan Asia, while the US outlook also improved, explain the economists.

NAB has an Australian GDP forecast at 1% in 2009 (essentially a strong Q4 expected as per the survey) and increased its expectation for 2010 to 3% from 2.75% previously. The economists are of the view that unemployment has peaked in Australia and the rate is now expected to fall to 4.75% by end 2010 and 4.25% by end 2011.

The RBA expected to increase in February and then pause to assess. NAB economists have changed the timing of expected rate rises in 2010 to May, August, and November, but they still see the official cash at 4.75% by end 2010. The official cash rate is projected to peak at 5.50% in mid 2011. Inflation forecasts have increased to 2.3% by end 2010 reflecting a tighter labour market.

Turning to the December survey in more detail, NAB reports business confidence fell significantly in December - down 11 to +8 points - but remains above long term averages. Comment the economists: “The fall may represent a return to greater realism given current activity and trading conditions”.

Overall, they highlight, the falls in confidence were broadly based, though more marked in retail, transport and personal and recreational services. This, they add, suggests that RBA actions in combination with the high AUD are starting to moderate expectations.

Business conditions remained unchanged at +10 index points in December. Trading and profitability both improved marginally; by 2 and 1 points to respective readings of +17 and +12 points. A more marked improvement was evident in labour conditions, with the index up 5 to +7 points (indicative of continuing labour hiring).

Business outcomes across sectors were mixed. Retail, wholesale and especially personal and recreational services reported significantly weaker outcomes, but transport, finance and business services, and to a lesser extent manufacturing improved.

Forward orders edged back somewhat (down 2 points) to a still strong +7 index points, with the economists pointing out this follows sharp improvements in recent months. NAB economists believe the December read remains broadly consistent with domestic demand increasing by around 4.75% in the second half of 2009.

There was also no sign of de-stocking with the index broadly unchanged. Consistent with the general on going strength in demand capacity utilisation improved further by 0.2 percentage points to 81.6%. NAB reports the level is now above longer term averages and still clearly trending up. Against that exports continue to remain weak with the index at minus 13 points. Capital expenditure also edged down marginally but there has been some moderate improvement in longer term investment intentions.

Labour costs increased again: up 0.5% on a quarterly basis (0.9% last month). The economists highlight there has now been a six month run of faster wage increases, albeit the annual increase remained low at 0.6%. Purchase costs, surprisingly, increased by 0.6% in December (0.1% last month) albeit the 12 months to rate slowed further to 1.5%.

Economy wide inflation was unchanged at 0.3%, with the 12 month to rate slowing to 0.6% (0.7% previously). Retail prices were flat in December, with the economists speculating this is probably reflecting weaker sales, with the annual rate slowing to 2.4% (2.8% last month).

Credit availability improved in December, with the difficulty in finding finance index at 5 points (11 previously). Those not wanting finance edged higher to 37% from 34% last month.