FYI | Apr 04 2011

– BIS Shrapnel expects Oz annual engineering construction spending to top $100bn

– Civil work will increase by 20% in both 2011/12 and 2012/13

– Mining-related work to double by 2014

By Chris Shaw

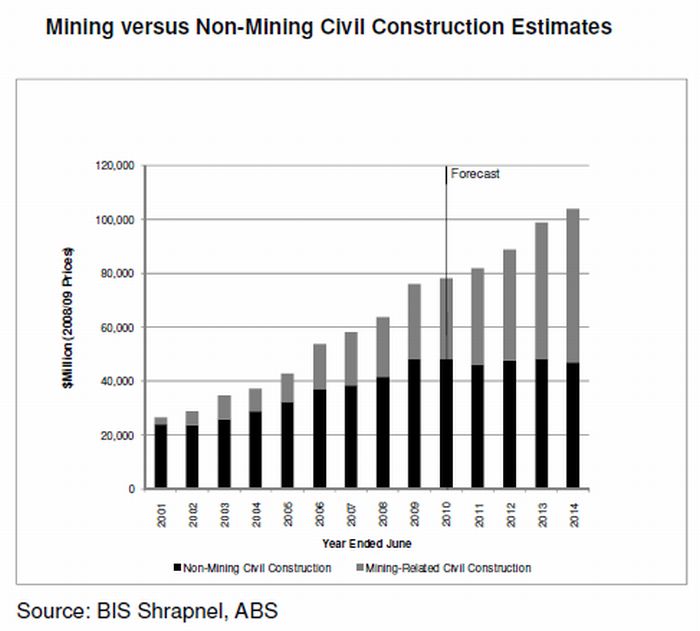

Australian civil construction activity is forecast to increase by 25% over the three years from 2010/2011, this according to a report by industry analyst and economic forecaster, BIS Shrapnel. The BIS report – “Engineering Construction in Australia 2010/11-2024/25”, suggests annual activity in the sector will for the first time exceed $100 billion.

According to the newest sector update, civil work done will increase by about 20% in both 2011/12 and 2012/13. This increase should be driven by a strong lift in both mining and LNG-related works and flood reconstruction activity in Queensland.

The expected gains compare to growth of just 2.8% in 2009/10 and a forecast 5.0% in 2010/11.

The subdued growth in 2010/11 in particular reflects the completion of a number of existing projects, as well as delays in ramping up the next round of mining-related works in particular. Beyond this year, BIS infrastructure and mining unit senior manager Adrian Hart sees the civil construction outlook as broadly positive as projects have been approved and momentum begins to pick up.

Hart estimates mining-related work, which includes mines, ports, railways and other infrastructure, will almost double between 2010 and 2014. This should see total work in this area increase to around $57 billion annually.

In contrast, annual work done on non-mining civil infrastructure, with the exception of railways, telecommunications and electricity, is forecast to decline to around $46 billion over the same four-year period.

This decline reflects moves by both Federal and State governments to rein in infrastructure spending in an attempt to strengthen their respective financial positions. As well, Hart notes private finance for such infrastructure projects remains constrained.

Hart expects reconstruction work in Queensland will see public sector funded work rise marginally in 2011/12, before again drifting lower in subsequent years. Again, Hart expects it will be the completion of current projects that contributes to the subsequent decline in activity.

Given such a view, Hart notes the outlook for civil work is significantly different than the pre-GFC period, as at that time both public and private funding were very strong. Hart expects the lack of a public sector driver will mean broadly weaker civil construction growth rates across the next four to five years.

Hart also takes the view skills shortages, project delays and further project cost increases will remain a feature in coming years. These factors are expected to constrain growth.

On a state-by-state basis, BIS expects there will be reasonable growth in New South Wales engineering construction activity in both 2010/11 and 2011/12. This will be driven by roadworks, rail and heavy industry, especially coal.

In Victoria, BIS is forecasting a significant decline in total activity in both 2011/12 and 2012/13, this reflecting the completion of the Wonthaggi desalination plant. This will hide some increases in activity in most other sectors, while by 2013/14 stronger growth should emerge as new rail, electricity, mining and heavy industry, harbours and telecommunications projects get underway.

Over the next five years BIS expects Queensland will see the largest rise in engineering construction projects, driven by flood reconstruction activity along with large LNG and coal projects. Across the next four years Hart is forecasting a 50% increase in Queensland's activity levels.

Completion or near completion of a number of major projects in South Australia should mean a move to lower activity levels through 2011/12. From 2012/13, BIS expects another substantial upswing in activity will get underway. This assumes a major expansion at Olympic Dam gets underway.

The Olympic Dam project will help drive increased activity elsewhere, Hart expecting a pick-up in associated work on ports, railways, roads, electricity and water projects. If Olympic Dam's expansion doesn't proceed, growth in activity in South Australia will be weak.

The completion of existing projects in Western Australia suggests flat growth in 2011/12 according to BIS, before stronger growth from 2012 through 2014 as activity on PNG and iron ore expansions peak. Hart sees the key risk for WA being the possible loss of skilled workers to support the expected boom in activity in Queensland.

Tasmania recorded a small decline in activity in 2009/10 but Hart expects strong growth over the next three years thanks to road, telecommunications, electricity and heavy industry projects. Similar strong growth in Northern Territory activity levels is expected, this driven by new LNG and oil projects.

Engineering construction activity in the Australian Capital Territory is currently growing very strongly thanks to the Cotter Dam and related water projects and some road and NBN (National Broadband Network) related work.

Hart takes the view activity in the region will decline sharply from 2012 as these projects are completed. This decline will come despite an increase in NBN-related works.

Technical limitations

If you are reading this story through a third party distribution channel and you cannot see charts included, we apologise, but technical limitations are to blame.