International | May 05 2017

By AtlasTrend

When you think about beauty products, your initial reaction may be of extravagant skin care or perfumes that are considered luxury items. However, the global beauty industry also encapsulates personal care products such as men’s grooming, deodorants and sun care products making it a large, diverse industry. Furthermore, consumer behaviour has changed dramatically over the last two decades with the rise of the internet and social media, particularly as social demographics have also shifted.

In this article, we will take a closer look at the global beauty industry, examine some of the trends that are occurring in the industry and see which companies will potentially benefit from these trends.

Industry snapshot

The global beauty industry is a large and diverse one with an array of global players but also remains relatively fragmented with regional players and many successful niche brands. It is worth US$370 billion and almost 75% of the industry is made up from the four largest categories: (1) skin care 28%; (2) hair care 18%; (3) make up 15%; and (4) fragrances 12%.

As the chart above details, the global beauty industry also includes personal care products such as men’s grooming, deodorants and sun care products.

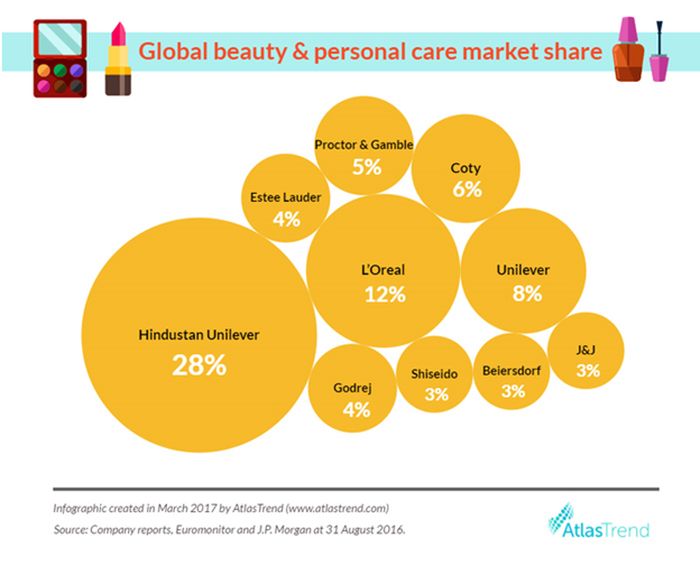

The industry is led by some significant global players, who focus on different parts of the industry. L’Oreal (OR FP) has a 12% market share, Unilever (ULVR LN) 10%; Coty (COTY US) 6%; Procter & Gamble (PG US) 5%; and Estee Lauder (EL US) 4% with all remaining players having market shares of 3% or less. Of course, both Unilever and Procter & Gamble are global consumer products businesses with only 38% and 17% of their sales in beauty, whereas the other three major players are focused exclusively on beauty products, as are companies such as Shiseido (4911 JP) and Revlon (REV US).

Industry growth and underlying trends

Surprisingly, growth in the beauty industry has slowed to 4.5% to 5.0% towards the lower end of the range since 2002, with the exception of the period during the global financial crisis (2008 and 2009) after it peaked in 2007 at just over 6.0% growth, according to Euromonitor. Whilst developed markets have largely ranged between 2% to 4% growth during the same time frame, it has been emerging markets that have largely driven growth in the industry ranging between 10% to 12% per year. However, growth has slowed to 8% over the last three years in emerging markets. History has shown that industry demand also follows economic or GDP growth cycles even at the prestige end of the market.

However, what is most interesting is which segments of the beauty industry are growing and why. For much of the 2000s decade, skin care had been the primary growth segment in the beauty industry where it averaged growth of 6% to 7% per year as it benefitted from the structural trend of an ageing baby boomer population and their associated wealth status. Growth rates have slowed to 4% to 5% since the global financial crisis whilst make up has the opposite performance and is now growing at 6% to 7% per year.

There are several reasons for this structural shift:

- Since the global financial crisis, consumer behaviour has become more conservative in spending on discretionary items. Make up is generally more affordable than skin care products and therefore, more resilient in slower economic times even though it is still considered a ‘luxury’ item for many consumers.

- Instant gratification has played a major part in how consumers behave as make up achieves quicker or instant results than skin care, which is more focused on long term benefits. As Estee Lauder has noted:

“The 30-year-old today gets more photographs of themselves in a day than their mother did in a year, so they care about what their skin looks like now, not when they are 40.”

This quote also explains how social media has also had a significant impact on consumer behaviour where it is also being used by companies (either directly or through social influencers) to guide consumer preferences and trends. This is especially the case with the younger generation of millennials, who are spending more time on social platforms and photo apps such as Instagram, Snapchat and YouTube.

Other areas of growth in the beauty industry include men’s fragrances, deodorants and men’s grooming, which are also being driven by the growing millennial population as well as strong demand from Asia. There is also a growing social consciousness about the use of more natural ingredients and this has led to demand for more organic-based products and the success of brands such as Vogue International’s natural shampoos and L’Oreal’s Elvive range as well as newly created celebrity brands by the likes of Jessica Alba (Honest Beauty) and Australia’s Miranda Kerr (KORA Organics).

Finally, the large global players such as Estee Lauder and L’Oreal with a focus on premium brands have also performed relatively well compared to those more focused on mass market products.

The industry leaders

The last 15 years has seen consolidation by the global players as they seek growth in faster growing market segments. In fact, these top 15 global leaders have had to continually make acquisitions just to maintain their market share of about 50%. Some recent and notable examples include Coty’s US$12.5 billion acquisition of 41 of Procter & Gamble’s beauty brands; Revlon’s US$870 acquisition of Elizabeth Arden; L’Oreal’s US$1.2 billion of IT Cosmetics; and Johnson & Johnson’s (JNJ US) US$3.3 billion acquisition of Vogue International, a natural hair care business.

Meanwhile, the industry has also seen a proliferation of new brands, focused on regional demand or product niches. These smaller players have continued to emerge and grow. Some of the reasons for this trend include:

- Lower barriers to entry afforded by technology and the internet. Like many industries, this has heavily impacted the marketing and distribution of products, where these brands have utilised digital marketing and direct methods of distribution to overcome the larger budgets needed for traditional media spending and access to shelf space in department stores and supermarkets.

- Faster product development cycles where beauty products are being brought to market in 3 to 6 months compared to 12 to 24 months by the larger, global players.

- Millennials who are willing eschew traditional brand names for upcoming brands, particularly those with a niche, be it regionally specific (especially in Asia), an organic-based brand or being heavily endorsed by a social media star.

The large global players will continue to grow through acquisitions as they seek to fill gaps in their respective brand portfolios. Meanwhile, we believe some of the smaller or regionally based players provide the more interesting stories and who are well positioned for also organic growth. Potentially, some of these will also become acquisition targets for the large global players. We highlight some of these companies below.

L’Oreal

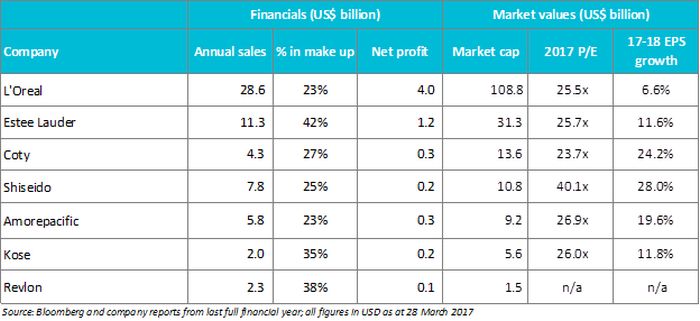

L’Oreal is headquartered in France and apart from its eponymous brand of L’Oreal, it also owns global brands such as Kerastase, Garnier, Maybelline, Lancome, Biotherm, Shu Uemura amongst many others. About half of its revenues come from premium brands as well as on make-up and skin care.

Estee Lauder

Estee Lauder was founded in the U.S. and is solely focused on the premium end of the beauty market. Apart from its eponymous brand, it also owns brands such as Clinique, MAC, Darphin and La Mer. About 80% of its revenues come from make-up and skin care.

Coty

Founded in France, Coty is now listed and based in New York. It is primarily focused on personal care products and haircare with brands such as Clairol, Cover Girl, Max Factor, Rimmel and Wella. About 60% of its revenues come from premium brands, 50% from make-up and skin care. It also has a significant fragrances business with brands like Marc Jacobs, Calvin Klein, Chloé, Gucci, Hugo Boss, Balenciaga Bottega Veneta, Alexander McQueen and Miu Miu. It has been highly acquisitive in recent years and is likely to make more acquisitions, particularly in faster growing emerging markets.

Shiseido

Shiseido was founded in 1872 with a primary focus on premium skin care and make up products. About 80% of its revenues come from premium brands, 70% from make-up and skin care and it sells about 65% of these products in Asia (40% in Japan) with the 20% in the Americas and 15% in Europe. It is beginning to expand outside Asia with acquisitions of premium skin care brands, Laura Mercier and ReVive.

Amorepacific

Tracing back its roots to 1932 in Korea, Amorepacific (002790 KS) owns dozens of Asian based brands with the most well-known being Laneige and Sulwhasoo. About 60% of its revenues come from premium brands, 90% from mostly skin care with a much smaller exposure in make-up. Just under 75% of its revenues are derived from the Korean market with China being its fastest growing market.

Kose

Kose was founded in 1946 in Japan and sells its make-up and skin care products primarily across Asia. About 80% of its revenues come from premium brands, 90% from make-up and skin care with a focus on natural ingredients. It also owns the Jill Stuart brand that it is rolling out through airlines and airports across the Asian region.

Revlon

Founded in 1932, Revlon produces make up, skin care, hair care, men’s grooming products, deodorants and fragrances under brands such as Revlon, Elizabeth Arden, Juicy Couture and other celebrity partnership brands such as Britney Spears and Christina Aguilera. It is considered more of a mass market brand with about 45% of its revenues coming from make-up and skin care.

Lastly, there are several large diversified companies with significant beauty businesses, primarily in personal care such as Unilever, Beiersdorf (BEI GR) and Henkel, (HEN3 GR). Despite owning many strong consumer brands, both Beiersdorf and Henkel have experienced market share losses due to maturing businesses, which also partially explains why Procter & Gamble made the decision to sell part of its beauty business to Coty in 2016.

Generally speaking, our preference would be to target the more niche, regional players who have better growth prospects particularly those exposed to the Asian region, where demand remains strong. With most, if not all, these companies attempting to grow their make-up businesses, it appears consolidation in the industry will be ongoing, particularly of smaller (largely privately held) brands.

We believe current valuations appear too high given the growth profile of the industry and the underlying companies. A case in point is Coty – although earnings per share is forecasted to grow 24.2% in 2018, it is largely due to its recent acquisitions. However, 1H 2017 has demonstrated that the company is still dealing with integration issues as well as falling sales of its existing businesses, where like-for-like sales fell 9%. Until we see better growth prospects, we will prefer to remain on the sidelines on Coty and the rest of the industry.

Content included in this article is not by association the view of FNArena (see our disclaimer).

If you are reading this story through a third party distribution channel and you cannot see charts included, we apologise, but technical limitations are to blame.

AtlasTrend is a global equities fund manager that makes it easy for anyone to invest in the world’s most thriving trends. The team brings a wealth of investment insights and access to smart and hassle-free global investing through an engaging and fully transparent online investment platform. To gain more actionable investment insights from the AtlasTrend team on profitable world trends (such as the growth of online shopping or rise of big data) and the listed international companies benefitting from these trends, register today for a free trial at www.atlastrend.com.

Important notice

Atlastrend Pty Ltd (ABN 83 605 565 491) is a Corporate Authorised Representative (No. 001233660) of Fundhost Limited (ABN 69 092 517 087, AFS License No. 233045). Any advice contained in this communication is general advice only. None of the information provided is, or should be considered to be, personal financial advice. The content has been prepared without taking into account your personal objectives, financial situations or needs. If you consider it necessary you should seek your own advice before making any financial or investment decisions. The information provided in this communication is believed to be accurate at the time of writing. None of Atlastrend Pty Ltd, Fundhost Limited or their related entities nor their respective officers and agents accept responsibility for any inaccuracy in, or any actions taken in reliance upon, that information.

Any managed investment fund product (Fund) mentioned in this communication is offered at www.atlastrend.com via a Product Disclosure Statement (PDS) which will contain all the details of the offer. The PDS is issued by Fundhost Limited as responsible entity for the investment fund products. Before making any decision to make or hold any investment in a Fund you should consider the PDS in full. The PDS is available at www.atlastrend.com or by calling AtlasTrend on 1800 589 778. Investment returns are not guaranteed. Past performance is not an indicator of future performance.

Find out why FNArena subscribers like the service so much: "Your Feedback (Thank You)" – Warning this story contains unashamedly positive feedback on the service provided.