Feature Stories | Aug 08 2007

By Greg Peel

Subprime, subprime, subprime – it’s all you ever hear at the moment. World financial markets are in a crisis (the ASX 200 has been down over 8% from its high) and the catalyst for the crisis can be traced back to the US subprime mortgage market. Fortunately for Australia, there are comparatively few subprime mortgages on issue, ergo Australia, while suffering some short term pain, is actually immune from any ultimate disaster.

Or so the story goes.

National Australia Bank CEO John Stewart said of the US subprime crisis when speaking on the ABC’s Inside Business program on Sunday:

“It’s very serious and it’s got a lot further to go, it’s about 15% of the mortgage market in the US. To give you an idea, that is about US$1.3 trillion . Right now about 20% of it is in arrears.”

But could Australia suffer a similar crisis?

“Similarities (are) next to nothing, there’s 15% of the market there, less than 1% of the market here. The implications for Australia luckily are quite small because there’s no direct effect in Australia”.

Yes it is lucky. For if it were unlucky, one presumes Macquarie Bank shares would have fallen in value a lot more than the near 25% they have so far. But Macquarie Bank has been at pains to point out that the bank has no direct exposure to the US subprime mortgage market. Just as well.

How did America get itself into this situation?

Dr Steve Keen, Associate Professor of Economics & Finance at the University of Western Sydney, has a straight forward view:

“The story with America’s [recent] stock and housing markets is that the vast majority of share and house purchases do not actually add to America’s stock of either businesses or houses. Instead, they shuffle ownership of pre-existing assets on a secondary market, with sellers attempting to realise speculative capital gains, and buyers entering on a rising market, anticipating further capital appreciation in the future. The whole process is fuelled by borrowed money.”

And the result, notes Dr Keen:

“The Sub-Prime Boom was a means to make money by lending money to people who couldn’t afford to repay it. It didn’t actually work? Well blow me down…”

The essence of the problem is that more and more borrowed money was being used not to finance the production of new assets, but to allow some speculators to buy existing assets from others, says Dr Keen. Those who got in too late, or didn’t get out in time, were simply adding to society’s general suffering, for while the debt repayment increases there’s little or nothing to show for the additional debt. Debt-financed spending enabled credit-fuelled purchases of commodities and services. But debt grew much faster than the increase in output it spurred, simply because most of the debt was not being used to actually build future productive capacity.

In the case of mortgage securities, there was no new asset created. Existing loans were simply being repackaged and sold off to speculative investors such as hedge funds, who leveraged many times (borrowed more) to fund their purchase. The demand for such investment products pushed mortgage lenders to sell more and more loans, and as the prime mortgage candidates all bought the houses they wanted there was nothing left to do but start giving mortgages to subprime candidates. These newfound holders of credit then went into the market not to buy from an abundance of newly built houses on offer, but to mostly buy an existing house for a higher price. Thus as house prices pushed ever higher, it was only a matter of time before the truth came out – that subprime mortgage candidates are subprime mortgage candidates because they simply can’t afford a real mortgage. To wit, there was a very good chance they could never ultimately make the payments.

As soon as the inevitable defaults began, house prices unsurprisingly began to turn around. House values then fell below mortgage values and we pretty quickly spiralled down to the crisis the US now finds itself in.

“Only in the aftermath, “says Dr Keen, “has it become obvious to all and sundry, that what drove the apparent prosperity while the Schemes were afoot was not financial genius, or brilliant innovation, or sterling industry – the usual suspects of the financial pages while the boom lasts – but reckless lending and borrowing.”

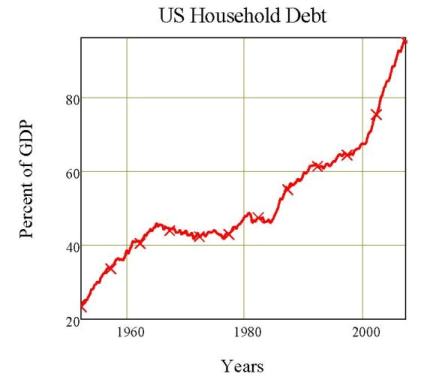

In the mid-eighties, US household debt stood at 46% of GDP but jumped up to 56% by the time of the stock market crash of 1987. The rate of growth then slowed until after the dotcom crash of 2000 at which point the US government turned on the liquidity tap to reignite the economy. Today US household debt stands at 95% of GDP.

It is no great surprise that the acceleration of Australia’s private debt has plotted out a similar path. As global interest rates were lowered when the US attempted to reignite its economy, so too did interest rates in Australia fall to levels that had not been seen in decades. The result was a concurrent surge in household borrowing.

But Australia has nothing to really worry about, of course, because as John Stewart has pointed out, and as Peter Costello has pointed out, and as many other bankers, brokers and politicians have pointed out, Australia, unlike the US, has an inconsequential subprime mortgage exposure.

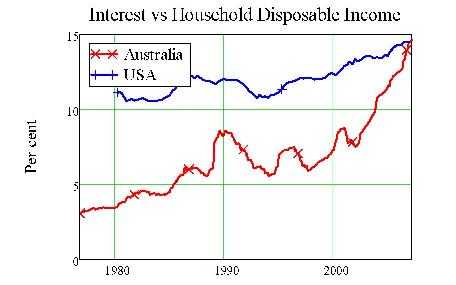

It should thus follow that if the Americans are far more exposed to subprime mortgages then the level of interest payments as a proportion of disposable income for US borrowers must be much higher than it is for Australians. A greater percentage of Americans took out mortgages when their incomes did not duly justify such loan repayments. However, this does not appear to be the case:

Nevertheless, it is the subprime mortgage holders in the US that are defaulting as we speak and because Australians do not have such a high level of subprime mortgages then defaults in Australia must logically be comparatively inconsequential. Once again, everyone is telling us not to worry. But it seems that not everyone has been quite so circumspect about the potential for a fair bit of mortgage pain in Australia as well – subprime or no subprime.

It was the end of February this year when the world was first to learn of any problem in the US mortgage market. It took a sharp fall in the Chinese stock market at the end of the month to spark a rapid divestment of risky assets and expose exactly just what level of vulnerability existed in the US credit derivatives, particularly subprime CDOs. But blissfully unaware of what was about to occur, Tim Brown, head of Macquarie Bank’s mortgage arm, spoke to ABC Radio’s AM program on February 12:

“The biggest pressure of course is the last interest rate increase in November which is only just now starting to filter through to people’s home budgets and I think now that they’re starting to get the impact of that, they’re having to reorganise their spending habits and obviously reduce their outgoings to cater for that.”

Before there was any talk of mortgage crises, the average Australian borrower was already reeling from three interest rate rises in 2006 when household budgets were stretched to the limit and borrowings were at maximum levels for many. Macquarie Mortgages commissioned a survey of 900 mortgage brokers, financial planners, accountants and lawyers in late 2006 to gauge the health of the property market. ABC reporter Peter Ryan learnt the findings:

“And the news is not good. According to the survey prices are stalled and sales are down. And some home owners are crumbling under the weight of debt they can no longer service.”

Tim Brown noted that 61% of professionals surveyed in February expected mortgage stress and mortgage defaults to increase this year as highly leveraged households grappled with a painful reality check.

“I think they’re stretched now in many cases, another one [interest rate rise] I think could crucify a number of families.”

By June of this year, we had learnt all about US subprime mortgage problems, but the panic that had followed February’s scare had abated and stock markets were surging back to new highs once more. But beneath the surface of the Australian mortgage market, little had changed:

“Australia’s leading mortgage insurance companies are reporting higher home default levels following a massive increase in lender mortgage insurance claims. Accounts filed by the two major mortgage insurers with the Australian Securities and Investments Commission (ASIC) showed both were hit by the increase in claims. Mortgage insurance claims are a leading indicator of any changes in credit quality brought about by rising interest rates and falling property prices. ‘Having had a seven-year period of favourable conditions the decline we’re now seeing in home loan affordability has brought our default experience in line with long term trends,’ said PMI [mortgage insurers] chief executive Ian Graham.” (Herald Sun)

Then in July, all hell broke loose. It started with two Bear Stearns debt funds, and has so far grown to impact Basis Capital, Absolute Capital, and two Macquarie Bank debt funds in Australia alone. To date it has impacted on the UK’s HSBC, France’s AXA and forced the rescue of German lender IKB. The Australian stock market has fallen by 8%, and all global markets have fallen by similar numbers. It is still being called the “US subprime mortgage crisis”. Is that still all it is?

No it is not.

This is now a global credit crunch. You can still call it “The global credit crunch that started in the US subprime market”, but then that’s like calling World War II “The war that started when Poland fell”.

Part of the reason the US stock market and global stock markets have been so weak is that credit lines have dried up in the private equity leveraged buyout market. According to Barings Asset Management, tightening debt markets have forced some of the world’s largest lending banks to shelve planned issues of corporate loans and bonds worth US$43 billion in the last two weeks. The fear is that if you take merger & acquisition activity out of global stock markets, there is no reason for stock valuations to be anything as high as they have become. M&A activity, and particularly LBO activity, has been a driving force in the global equity rally of the past two years. The value of corporate issues shelved by banks last year was exactly none.

What is the connection between a low-income-earning American with a mortgage he should never have been given and the potential failure of a multi-billion dollar buyout of a US blue chip stock? Well there should be none, but there is. For our low income borrower has started a downward spiral that is now manifestly increasing the cost of borrowing and reducing the availability of credit for all financial activities. The higher the cost of borrowing, the lower the demand for any asset – property, equity, commodity. The lower the demand, the lower the value. While the jump in credit spreads is being viewed as a healthy “return to normalcy” by many, it does not represent a temporary shift

Alan Moss, CEO of Macquarie Bank, was quick to point out last week that the 25% losses being experienced by two of its funds occurred despite any exposure to subprime mortgages. It was just that without anyone currently prepared to buy leveraged debt securities of any quality, the apparent prices of such securities have fallen. The CEO of Absolute Capital had made the same observation the week before, when freezing redemptions. Absolute has only 5% exposure to subprime securities, but were it forced to sell its higher quality assets into an unwilling market it would be technically insolvent.

Unlike Basis Capital, which really did have significant exposure to subprime securities, both CEO’s above expect a return to normal trading once the subprime dust can settle.

Unfortunately the dust was never going to settle fast enough for US lender American Home Mortgage, which filed for bankruptcy last Friday. For AHM’s problems stemmed not from problems in subprime mortgages, but from problems in “alt-A” adjustable rate mortgages, which FNArena has previously described as “mezzo-prime”. Such mortgages are reasonably familiar to Australians as they offer interest rate “honeymoons” initially before later significantly adjusting upward in required interest rate payments. There have been over US$1 trillion of such loans written in the US to date, and most begin their painful adjustment in the next few months.

While alt-A mortgages are considered of a better quality than subprime mortgages, the popularity of both was undoubtedly driven by the same three factors: (1) mortgage lenders were keen to write them; (2) they meant being able to afford a house, or perhaps a bigger house, than previously and (3); if the mortgage payments became too much the borrower could either sell the house, or refinance it, at a higher value (for the market was booming).

The same concept lay behind so-called “prime equity loans”. These loans have also been popular in Australia, and involve homeowners taking advantage of the increased equity value in their house (driven by the property boom) by borrowing against that equity and spending it elsewhere. What about buying some shares perhaps? But of course the same obvious problem overlays all these forms of borrowings. They all rely on the value of the mortgaged property either increasing in value or at least not decreasing in value.

On July 25 America’s largest mortgage lender – Countrywide – announced a fall in second quarter profits of 33%. The problem was not subprime lending, and although there was some pain it wasn’t even alt-A lending either. It was mostly prime equity loan lending. This was the point at which the US stock markets really turned tail. The subprime crisis had become prime.

So now let’s come back to Australia again – the land where subprime mortgages are clearly not an issue.

The housing market in Australia had begun coming off the boil before the US slump began (and indeed the Australian housing boom began ahead of the US). The extent of slump in Australia has not been hugely disastrous, if for no other reason than state-by-state figures have tended to net out. Sydney housing had been the first to skyrocket, as Sydney is Australia’s biggest city and a nice place to live by global comparisons. But even as Sydney prices had begun to fall prices in Perth had only begun to take off, as Perth is a beneficiary of the Western Australian mining boom.

But as we learnt earlier from Macquarie’s Tim Brown, problems in the Australian mortgage market had set in even before anybody had heard of subprime loans. By June, as we learnt from PMI’s Ian Graham, the problem appeared to be worse. The epicentre of Australia’s current mortgage problem is Sydney’s sprawling, low-income western suburbs. But last week West Australian Newspapers, which has a virtual monopoly on Perth’s property classifieds, announced a profit that surprised some brokers. The increase was put down to higher than expected number of property ads. It would seem there is an increase of houses for sale in Perth.

While the bankers, brokers and politicians are telling us there is nothing to worry about on the Australian housing scene, mortgage lenders are teetering. Banks will be rapidly tightening their lending practises, both to their own mortgage customers and to the independent mortgage lenders they also finance. If you are looking to get a housing loan in Australia this month, you’d better have your documents in order. For there is little chance any mortgage lender will be giving you money to buy a house right now unless your bona fides are extremely bona.

There was the slightest hint the Australian property market was starting to pick up a bit a month or so ago, particularly in the area of Sydney investment property. It is difficult to see this move gaining any sort of momentum at present, and indeed it is more likely the tightening of global credit and the wake-up call to over-exuberant mortgage lenders will impact on mortgage availability and cost, and this will in turn lower the demand threshold for homebuyers.

And on Wednesday we may get an interest rate rise. If not for the fallout from the “US subprime mortgage crisis” it would be a given that we will get an interest rate rise, given the raft of recent inflationary data. There is little doubt that if we do get an interest rate rise, Australia’s own mortgage woes will step up a gear. In Dr Steve Keen’s opinion:

“Here I believe that the RBA is playing with fire. I have no doubt that, at the moment, increasing interest rates will dampen inflation. My concern is that an interest rate rise will have a far greater depressing impact on the economy than the RBA anticipates, because its models ignore the role of debt.”

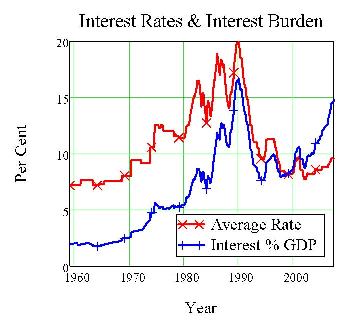

Dr Keen notes that interest payments on private debt currently consume 14.77 cents in every GDP dollar. If the RBA increases rates by one quarter of one percent on Wednesday, the interest payment burden will break through the 15 cent barrier to be 15.27 cents per GDP dollar. There are only 15 months in Australia’s economic history where this burden has been higher: between May 1989 and July 1990. Therein followed the “recession we had to have”. Considering that the inflation rate reached as high as 18% preceding this recession, and that it is below 4% now, Dr Keen questions the RBA’s obsession with fighting inflation in the current debt environment.

For despite Australia’s immunity to subprime mortgages, the evidence would suggest a new round of delinquencies and defaults will surely follow an interest rate rise. And with a global credit crunch going on, probably irrespective of a decision not to raise.

Which brings us to a topic that has been receiving a lot of electioneering interest of late – housing affordability.

The politicians and bankers can bang on as much as they like, but the truth is housing affordability is simply a function of demand and supply. It has little to do with monetary policy per se, and absolutely nothing to do with ludicrous and overtly political government initiatives like the $7,000 first homeowners grant, which immediately pushes the price of every eligible dwelling up by $7,000. Nor does stamp duty make the slightest bit of difference, for to reduce or abolish stamp duty only has exactly the same effect.

The pervading level of interest rate makes little difference, for in a high interest environment the higher cost of payments mean buyers will pay less for a house, and in a lower interest environment they will pay more for a house. Zero sum.

Investment property buyers can push the affordability issue around a bit, but it must always return to the mean. For if too many investors enter the market there is a glut of rental property available, and rental yields will fall thus rendering investment property unattractive again. And despite an extraordinary passion among Australian investors for negative gearing, the fact is, was, and always will be that if your property is negatively geared you are losing money. Take away the negative gearing tax break, and you will just produce another fiscal shift in the value of a property.

Obviously the affordability of a house is a function of the number of houses in supply, and the increasing population from both births and immigration. Given the birth rate effect is a function of 20-30 year-old policy, there’s not a lot you can do about that to take immediate measures. Immigration can be crimped, but then we need skilled workers for our economic boom. So really you just have to build new houses, or turn old ones into apartment blocks, and the problem will quickly be solved.

But if Sydney is a good proxy for the whole country, hands up anyone who hasn’t noticed that the last time you drove to Goulburn there was ten minutes more of western sprawl than previously, and that you could have sworn that you filled up at the service station which is now a block of units only a month ago. There are plenty of dwellings being built – too many if the environment is to survive but that’s another story.

So how come housing is so unaffordable?

Aussie Home Loans founder John Symond has a bee in his bonnet about it, he being the king of making housing affordable for Aussie battlers back in the nineties. He agrees that any fiscal measures are “band-aids”, and he is frustrated that no politician is coming up with anything useful. Commonwealth Bank CEO Ralph Norris is also up in arms.

Oh how exquisite the irony. (And this has got nothing to do with each of these commentators’ own castles).

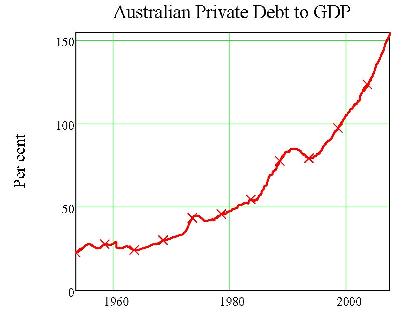

Now take this graph:

Draw a line through the first three X’s and then a separate line through the last three X’s and you will notice a distinct shift in growth acceleration of Australian mortgage debt. Where does the shift take place? Just about where Aussie John introduced mortgage securitisation to Australia. In making home loans more affordable for Australians, Aussie John issued in a new era where mortgage availability was no longer under the control of traditional banks with simple deposit-loan ratios and a lender of the last resort facility from the RBA. Mortgage availability became a financial market function of competition and profitability well beyond the constraints of the four pillars and 100 years of tradition.

Mortgages became cheaper as a result. So what’s the next screamingly obvious thing that’s going to happen? Yes, the great housing boom began. And well may Ralph Norris scoff, as his bank joined the rush to lend to mortgage originators and to compete with Aussie and its overnight clones in equal measure. And to invent ever more accessible mortgages and home equity loans. Throw in a collapse in world interest rates brought about by the dotcom bust and 9/11, and you have a recipe for a house price bonanza.

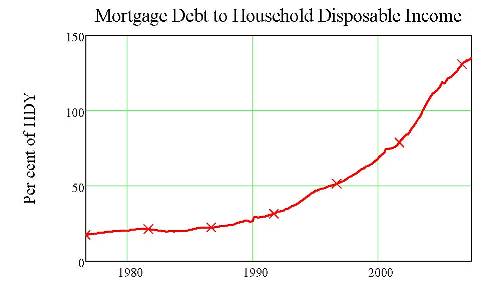

Not that it’s all Aussie John’s fault. For realistically the cheap mortgage/expensive house and low interest rate/expensive house equations balance. Affordability should remain fairly constant. Maybe the following graph provides a clue:

Notice how closely the blue line matches the red during the decade from Keating’s recession to the dotcom bust. Then have a look at where the two lines are now, and where they were when your parents bought a house. There is your answer, plain and simple.

Your parents were happy with a modest cottage. For today’s homeowners it’s a McMansion or nothing. Your parents had to have the bank manager over to dinner before he would even contemplate giving them a home loan. Today you can get a home loan (at least you could) over the phone from someone cold calling. There is only one reason Australian housing affordability is at an all time low and that is greed. Greed from the homeowners, and greed from the mortgage lenders. Greed is what causes bubbles, and too much greed is what bursts bubbles.

It’s nothing to be ashamed of really – it’s been happening since time immemorial. But every time a bubble bursts someone gets hurt. This time it will be the overstretched, over-borrowed, Aussie “aspirants” with eyes bigger than their wallets, and cowboy lenders with Ferraris and coke habits.

Subprime? It’s all just part of the same big market.

Note: All graphs courtesy of Dr Steve Keen. Dr Keen’s August DebtWatch available at www.debunkingeconomics.com and www.debtdeflation.com/blogs.