Australia | Jun 27 2008

By Greg Peel

In a lot of ways silver has been in recent decades the forgotten metal, struggling with an identity crisis as a poor man’s precious metal and/or a rather expensive industrial metal. In its glory days, Broken Hill in western New South Wales was known as Silver City, and to this day the highway leading into the town is so named. Broken Hill gave its name to a rather famous Proprietary, but these day’s when one thinks of BHP Billiton one doesn’t immediately think of silver, or for that matter the zinc and lead upon which the company built its foundations. Today junior mining companies are left to squabble over what commercial deposits may still remain at Broken Hill.

Indeed for many years silver became merely a helpful by-product of mining for base metals occurring, as it often does, in base metal deposits. Base metal miners could sell the silver just to keep a cash-flow going, or to finance mine expansions. In more recent years even the industrial value of silver has been under threat, given the world has moved to digital photography. However…

“Silver has the highest electrical and thermal conductivity of any metal, the highest optical reflectivity, and the lowest contact resistance. Silver is classified as a precious metal, but it is the only metal with the chemical reactivity to act as a catalyst in several applications. While ‘precious’, the vast majority of silver’s usage today is in industrial applications.

“‘Silver is arguably the most versatile of metals’, notes silver expert Richard Karn, ‘as is witnessed by more patents being filed for new uses of silver each year than for all other metals combined'”.

These excerpts come from a 2006 FNArena story “The Age of Silver” (Sell&Buyology: 24/11/06) which was later followed up with “The Age of Silver Revisited” (Commodities: 05/04/07). While the stories are now a bit dated, the fundamentals have not changed – silver is witnessing a rebirth. That rebirth has also been helped along by the introduction in the US of silver exchange-traded funds.

However, for those in Australia wishing to invest in silver through investment in local mining companies, the situation is problematic. Silver mining is either buried within the extensive operations of the large diversifieds, or, as aforementioned, is a by-product for base metal mining companies.

Malachite Resources ((MAR)) hopes to provide an alternative.

Malachite is a company with a market cap of $26m and has to date proven a successful mineral explorer. But it can now be classified as an emerging miner, with the intention of becoming, in the words of CEO Dr Garry Lowder, “a serious, dividend-paying, mid-tier mining company”. FNArena lunched with Dr Lowder recently and learnt all about the Conrad silver mine.

The Conrad mine is located near Inverell in the New England region of New South Wales. It was in operation as early as 1902, but was forced to close under union pressure in 1912. It seems the proprietors attempted to bring in a system of enterprise bargaining. Hmm. The mine was later reopened by then large mining company Broken Hill South, but was again abandoned in 1957 following the collapse of the lead price. With no incentive to mine for lead, clearly BHS also saw no value in pursuing the mine’s by-product – silver.

Indeed, Conrad is a “polymetallic” reserve, containing all of silver, copper, lead, zinc, tin, and a rare metal called indium. More on indium later. Malachite is now the 100% owner of Conrad, and the company is cashed up and ready and boasts institutional support on its share register. As the greatest potential lies in the mine’s silver reserves, Malachite’s share price has been tracking closely to movements in the silver price of late.

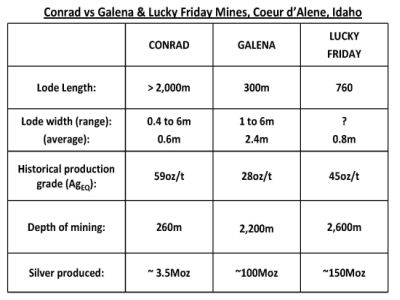

Dr Lowder describes Conrad as the sort of long term project most junior miners struggle to ever find. It is a “flagship project”, and “company-making”, he suggests. In order to appreciate Dr Lowder’s enthusiasm, attention is drawn to the following table.

This table compares Conrad’s specifics with the two famous US silver mines in Idaho, owned and operated by the world’s premier silver miner, Canadian company Coeur d’Alene. As the Conrad lode is longer, shallower, and boasts a superior historical production grade than these two globally significant mines, Malachite is very excited about the ongoing potential of its mine. Most notably, at only 3.5Moz produced to date, Conrad is offering potentially significant returns ahead.

The initial reserve estimate on Conrad is for one million tonnes of ore, to be recoverable at the rate of 20,000tpa. While this suggests a mine life of five years, the expected total mine life is really closer to ten years. At this stage, Malachite is suggesting three years before initial production.

However, part of the lode includes a section of very high-grade ore at the surface. This ore may well be recoverable as early as late this year, and thus provide ongoing funding for the bulk of the project. However, Malachite actually has another trick up its sleeve.

The company also lays claim to the Karaula tin deposit at nearby Elsmore. This is another high-grade mineral reserve, which is as good as sitting on the surface. This is also, like Conrad, another mine previously abandoned due to tin prices falling below commercially justifiable levels. However, in the last two years tin has been undergoing somewhat of a renaissance.

The reason for tin’s return to favour is its non-toxicity. There are only two non-toxic industrial metals, and the other, coincidently, is silver. Tin was once used as the preferred medium for the storage of food. Today we still refer to the “tin can”, although in modern times food cans have been made from tin-coated steel. However, tin’s resurgence began in earnest in 2006 when the European Union banned the use of lead in solder.

Solder is typically an alloy of tin and lead. But lead solder is now banned in Europe because of the environmental impact of electronic goods dumped into landfill. While only a tiny amount of solder is actually used in every computer, printer, mobile phone etc, the sheer number of goods produced in the world each year means a growing amount of tin and lead is being used. Now that lead is banned in Europe, and may one day be banned globally, electronic goods manufacturers are turning to other alloys for use as solder. In any other alloy, the proportion of tin required is much greater. Hence the recent surge in the tin price.

Malachite estimates Elsmore can produce 500-1000t of tin per annum for four to five years from a mine which may ultimately produce in the order of 3, 4, or 5,000kt. The total expected annual cash flow from the mine is in the order of $5-10m. And because there is already a mine in place, and tin lies on the surface, Malachite can start producing tin almost immediately.

What this means is that Malachite should have no need to turn to equity or debt markets to finance the three-year ramp-up of the Conrad silver mine.

And returning to Conrad, it was noted that the ore reserves also contain copper, lead, zinc, tin and indium, which provides it with an element of metal risk diversification. Malachite is particularly excited about the indium. Indium is a rare metal, the price of which has risen from US$50/kg to US$750/kg in the last five years. The reason is that every flat-screen television produced in the world today has, as a critical component, a combination of indium and, funnily enough, tin. It is estimated there is very little indium actually left in the world, thus making it one of the most critical short-supply metals.

To top things off, Malachite also owns additional copper and gold projects in Queensland, but it is the tin/silver combination which Dr Lowder is highlighting as the making of Malachite.

Malachite is set to announce a reserve upgrade in August, following which Dr Lowder expects the shares to be equivalently re-rated.