Australia | Nov 15 2016

This story features ANZ GROUP HOLDINGS LIMITED, and other companies.

For more info SHARE ANALYSIS: ANZ

The company is included in ASX20, ASX50, ASX100, ASX200, ASX300 and ALL-ORDS

The banks had a disappointing year, but much as expected. The issue of capital requirements and dividends continues to linger.

– Revenue growth lowest in 25 years

– Capital growth exceeds expectation

– Dividend cuts still forecast

– APRA draws out the pain

By Greg Peel

The Regulators

There are two phrases which have been hanging like Swords of Damocles over Australia’s banks now for over a year – “domestic systemically important”, colloquially known as “too big to fail”, and “unquestionably strong”. The quantification of these qualitative phrases will determine whether or not, and if so, by how much, the banks will have to raise new capital.

It is hard to believe that these phrases relate to something that happened eight years ago. It’s just as well we haven’t seen another GFC in the meantime. And there’s still a long way to go.

Heading into the November bank reporting season, it was assumed by all that the Basel IV international regulations setting out new capital requirements for too-big-to-fail banks would be known by year end, after which APRA’s additional capital buffer implied by “unquestionably strong” would quickly be quantified, likely by early 2017. But while Basel IV remains on track, all and sundry have proven to be wildly wrong about APRA.

Over the weekend, APRA sought to “dampen any enthusiasm” of a swift resolution to “unquestionably strong”. To make matters worse, APRA is assuming capital requirements under Basel IV will come in short of the average 9.5% level of tier one capital Australia’s big banks have built to in the interim, and has warned the banks “not to get excited”. The implication is APRA will in no way be as lax.

Rather than announce its own capital requirements immediately in the wake of the expected Basel IV agreement, APRA intends to spend another full year consulting with the industry. Thereafter it would be yet another year before the final rules would be in place. In other words, previously the banks hoped that by the time the May reporting season rolled around in 2017, they would know whether capital raisings would be required or not. Now they’ll in theory be waiting until late 2019, or eleven years after Lehman Bros collapsed.

As investors, we can view this as either a reprieve – we don’t have to fear capital raisings for another couple of years – or as an extension of uncertainty – the APRA Sword of Damocles will continue to sway on. The market’s response yesterday was positive. Bank sector analysts are not quite as sanguine.

The Reporting Season

Bank analysts do nevertheless agree that one of the highlights of the November bank reporting season, which saw ANZ Bank ((ANZ)), National Bank ((NAB)) and Westpac ((WBC)) report full-year earnings and Commonwealth Bank ((CBA)) provide a first quarter update, was a greater than expected capital build, to that aforementioned average of around 9.5%. It is a positive because most analysts believe the ultimate regulatory capital requirement will be in excess of 10%.

However, when analysts were writing reporting season wraps, they were still under the assumption we’d know the result by early next year.

And capital was about the only highlight of this season. With interest rates historically low, funding costs rising, competition in mortgage lending and term deposits rife, and political scrutiny intense, banks managed to post the worst revenue performance in at least 25 years, UBS points out. It’s disappointing given retail and business credit growth was actually quite robust – what Goldman Sachs describes as “a more normal credit environment”.

The earnings results were nonetheless roughly in line with expectations. All banks are fighting hard to keep their costs under control, although this has to be achieved at a time required investment in new technology is forcing costs higher. Bad & doubtful debts (BDD) continue to quietly rise but not alarmingly so. The share count dilution of dividend reinvestment plans (DRP), which hark back to the capital issue, meant earnings per share fell and returns on equity were lower.

Unlike the May reporting season this year, there were no “single name” shocks among BDDs. It seems it was just a coincidence that your Dick Smiths, Slater & Gordons and so forth were hitting the wall at the same time six months ago. Yet despite no big shocks, BDDs were higher, although the same “pockets of weakness” were largely to blame – mostly in the NZ dairy industry and in the Australian mining states.

As far as mining states go, we are yet to see whether the sudden commodity price revival will play out into a reduction in household debt problems in Western Australia and Queensland.

Bank analysts agree that after the long period of BDD reduction post-GFC, the trend has now turned, but a gradual increase is expected from here rather than any rapid deterioration in loan quality. There is also agreement the subdued environment for bank revenues is unlikely to change in a hurry.

This puts the focus heavily on cost reductions as a means of earnings growth. “We continue to believe that expense management remains the key driver of performance,” says Macquarie. “The ability to extract costs becomes more of a focus,” says Citi, “if banks are to maintain growth in pre-provision [for BDDs] earnings”.

Despite praiseworthy efforts to date, the banks are still having to deal with elevated costs brought about by the indisputable necessity to adapt to the ever more digitalised world. Attempts to reduce costs and increase efficiencies remain a case of paddling a canoe upstream, but brokers warn the banks simply have to try harder.

Of most importance to investors is the matter of capital. The two big questions, inexorably linked, are will the banks need to raise capital and will they need to cut their dividends. Or both.

Capital

The banks’ drive to pre-emptively increase tier one capital has pushed levels to above what analysts were forecasting at this November season, but has also dragged on earnings per share as the competition for deposits drives down margins and DRPs dilute the share count. The bad news is it may still be two years before we finally know what tier one ratios need to be, but the good news is the banks still have two years to get there, meaning the risk of another round of significant capital raisings next May is now likely off the table.

There is a bit of a twist to the tale.

It relates to changes to rules relating to risk-weighted assets (RWA). Aside from requiring higher levels of tier one capital, which is basically equity, APRA has also recently tightened the rules on just how much of their capital the banks can lend out to riskier ventures, such as investor mortgages. While the requirements have not proven as onerous as feared, how RWA ratios are measured comes down to the bank themselves, not to the regulator or any other independent assessor.

By lowering RWA ratios, banks improve their tier one capital. One way to lower RWA ratios is to reduce the number of risky assets. Another way is to deem the same assets to be less risky. UBS, for one, is suspicious that all of NAB, Westpac and CBA (first quarter) were able to improve tier one capital by RWA “optimisation” and “data improvements and refinements to parameters”. Only ANZ could show actual RWA reduction. This smacks a bit of conveniently moving the goal posts.

APRA has already declared “an increasing lack of faith in the use of internal models for calculating risk weights”. UBS therefore warns such “optimisation” may be unwound by either Basel IV initially or APRA’s interpretation of “unquestionably strong”. Presumably a “lack of faith” raises “questions”. Rather than requiring Australian banks to have a capital ratio 1% above the Basel requirement, it might be 2%.

Another way to increase capital is to reduce the amount of cash paid out to shareholders, meaning dividend cuts.

We recall that ANZ cut its dividend back in May. At the time, some brokers had expected other banks to cut as well, but they didn’t. Coming into the November season, all brokers agreed dividend payout ratios were elevated, some believed NAB and Westpac would cut and others believed they might wait until next May when the new capital requirements will be known.

NAB and Westpac didn’t cut, and we now know those requirements won’t be known. Assuming at the timing of writing its reporting season wrap the requirements would be known, Morgan Stanley forecast a 14% cut in dividend for NAB and 10% cut for Westpac in FY17.

That forecast is now clouded, but it does not change the fact payout ratios remain elevated, and therefore unsustainable in the face of increased capital requirements, whenever they may be settled upon.

Morgan Stanley is forecasting a required capital build of $14bn across the Big Four over the next eighteen months, with CBA requiring the most and ANZ the least. Goldman Sachs had forecast $14bn but has since reined that figure in to $8.8bn given the better than expected capital growth revealed in the reporting season.

Preferences

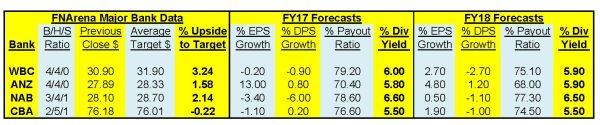

FNArena database brokers are split between whether the banks as a group are offering value or whether they are still worth keeping clear of. We might declare that balance a tight one, given there are eleven Buy ratings to thirteen Hold ratings among the eight FNArena database brokers, to only two Sells, as the table below shows.

Brokers are generally never keen to put Sell ratings on any stock and the downside floor of high yields makes Sell ratings even rarer for banks. Those brokers applying ratings on a more sector-relative basis rather than market-relative basis are nevertheless more open to Sell ratings.

What is clear from the table is either way, there’s little upside to consensus price targets left following the recent Trump rally, and indeed CBA has already exceeded its target (as of last night’s closing prices).

What is also clear from the table, compared to equivalent tables of previous times, is the large number of negative forecasts for earnings per share growth and dividends per share growth and also the fact there is no longer a single forecast dividend payout ratio of 80% or more, as had been the case for some time.

Technical limitations

If you are reading this story through a third party distribution channel and you cannot see charts included, we apologise, but technical limitations are to blame.

Find out why FNArena subscribers like the service so much: "Your Feedback (Thank You)" – Warning this story contains unashamedly positive feedback on the service provided.

Click to view our Glossary of Financial Terms

CHARTS

For more info SHARE ANALYSIS: ANZ - ANZ GROUP HOLDINGS LIMITED

For more info SHARE ANALYSIS: CBA - COMMONWEALTH BANK OF AUSTRALIA

For more info SHARE ANALYSIS: NAB - NATIONAL AUSTRALIA BANK LIMITED

For more info SHARE ANALYSIS: WBC - WESTPAC BANKING CORPORATION