Australia | Mar 24 2026

This story features MONADELPHOUS GROUP LIMITED, and other companies.

For more info SHARE ANALYSIS: MND

The company is included in ASX200, ASX300 and ALL-ORDS

Valuations for contractors and engineering companies are wildly different; a result of investors valuing execution over volume.

- Valuing contractors and engineering firms is no longer a one-size-fits-all exercise

- Proven track records of successful execution attract premium valuation

- Access to human capital is treated as a scarce and valuable resource

- Monadelphous' sector premium supported by gold standard status

By Paul Githaiga

The recent reporting season pointed to a shift long in motion: not all project backlog is valued equally. Revenue is there, pipelines are strong, yet valuation gaps are widening.

Part of this reflects “AIxiety” around white-collar work, but the real driver is scarce physical execution.

Investors are more willing to pay a “New Blue-Collar Premium” for contractors who turn work into cash reliably, maintain deep in-house teams, and deliver complex projects with precision.

In this environment, execution —not volume— is what creates lasting enterprise value.

The Taxonomy of the New Blue-Collar Premium

To understand the current market premium that is dividing the sector on the ASX, we must look beyond headline revenue and EBITDA.

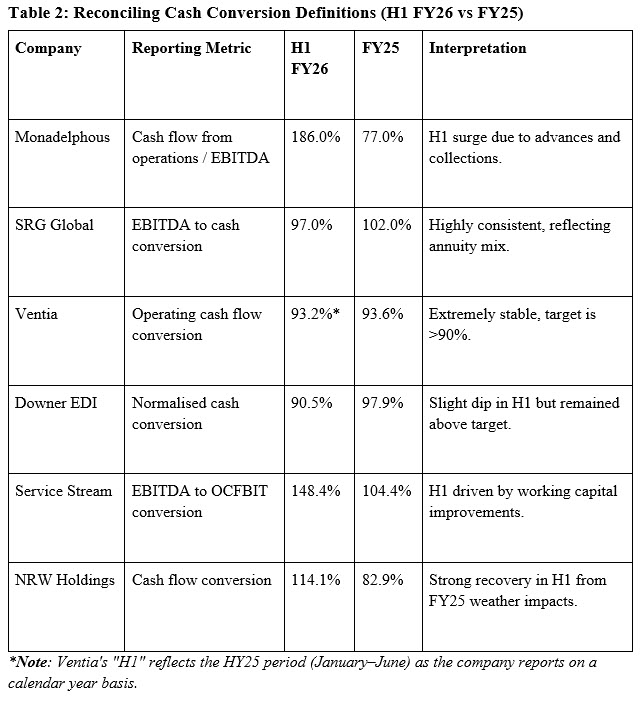

The key metric is the cash conversion ratio. It measures the efficiency of turning EBITDA into operating cash flow.

Sustained ratios above 90% indicate synchronised project management, milestone certification, and billing processes.

Ratios below this threshold often signal revenue trapped on the balance sheet due to rework, claims, or delivery friction.

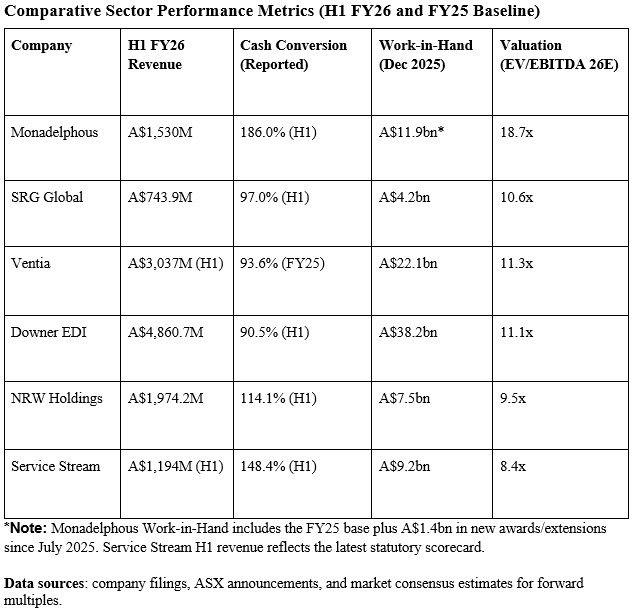

The forward multiples’ dispersion —from Monadelphous at 18.7x to Service Stream at 8.4x— cannot be explained by revenue or backlog alone.

Execution reliability, portfolio quality, and annuity-style revenue are now central to market valuation.

A Small Analytical Caveat

This is a small peer sample, so the conclusions are directional rather than absolute.

Company Profiles and Execution Insights

Monadelphous Group: Benchmark of Technical Specialisation

Monadelphous ((MND)) is widely recognised to be the sector’s gold standard.

H1 FY26 revenue hit $1.53bn, a 45.6% year-on-year increase, with a record 186% cash conversion.

This spike reflects both operational discipline and significant customer advances on new contracts, transferring financing risk from contractor to client — a privilege reserved for those with proven execution.

Divisional revenue growth underscores this capacity:

- Engineering Construction: up 67.2% to $677.8m

- Maintenance & Industrial Services: up 32.1% to $852m

Monadelphous maintains a direct-hire workforce of 8,389, providing both safety compliance and technical depth that acts as a barrier to entry.

In doing so, it captures the essence of the New Blue-Collar Premium: the market rewards its human capital as a scarce and valuable resource.

SRG Global: Annuity-Style Stability

SRG Global ((SRG)) demonstrates the premium in a mid-cap, capital-light context. H1 FY26 EBITDA rose 20% to $71m, with 97% cash conversion.

Its 80% recurring/annuity revenue profile reduces cyclicality and stabilises cash flows, exemplifying a predictable work-to-cash engine.

Strategic acquisitions like TAMS strengthen its market position in marine infrastructure, enhancing the execution premium.

Aggressive deleveraging and 20% dividend growth further cement SRG’s status as a reliable, high-quality operator.

Ventia Services Group: Defensive Scale

Ventia Services ((VNT)) is Australia’s largest essential services contractor, with $22.1bn Work-in-Hand and 93.6% cash conversion.

Its focus on higher-margin work and disciplined exit from low-margin contracts improved EBITDA by 13.3% despite modest revenue growth.

Long contract tenures (6.4 years average, 95% renewal) and a $250m buyback illustrate why investors assign an 11.3x multiple: predictable execution reduces risk and stabilises cash flows.

Downer EDI: Portfolio Simplification

Downer EDI ((DOW)) has re-rated its valuation by exiting non-core businesses, improving EBITA margins to 4.6%, and achieving 90.5% cash conversion.

This disciplined approach highlights the market’s recognition that the quality of earnings —not top-line growth— is the primary determinant of execution premium.

FY30 target of 6% EBITA margin shows continued alignment between operational discipline and market expectations.

NRW Holdings: Execution vs Volatility

NRW Holdings ((NWH)) presents a paradox: 114.1% cash conversion in H1 FY26 vs a low 9.5x multiple.

The explanation lays in project mix volatility — heavy reliance on contract mining and civil works, and a more variable delivery condition.

Strategic diversification via Fredon acquisition, with exposure to renewable, health, and data center sectors, positions NRW to capture the New Blue-Collar Premium once cash reliability is sustained across sectors.

To offer the full picture: shareholders in this company have had to endure multiple setbacks in recent years and exercise patience throughout multiple disappointing announcements.

NRW Holdings’ operational challenges were contract-specific rather than group-wide, with the first major pressure point emerging in FY23 as La Nina weather in Queensland, delayed project starts, labour shortages and cost inflation squeezed margins, particularly at Primero where fixed-price work was hit hard by cost escalation and labour availability.

The Primero issues ran deeper than site conditions alone, with NRW later restating FY22 after identifying a $10.3m revenue and margin overstatement on two completed projects, prompting tighter group-level oversight and management changes; by FY24, management was pointing to recovering MET margins as activity levels improved.

A second wave hit in FY25, this time in Mining, where profitability fell because of significantly higher-than-average rainfall in Queensland, the early termination of the Mt Cattlin lithium contract and reduced scope at Curragh.

The Curragh pressure appears to have been driven largely by the client’s own cost-reset, with Coronado Global Resources ((CRN)) disclosing the removal of five fleets from operation since April 2024 as it worked to cut costs and lift productivity.

Separately, statutory earnings were hit by the Whyalla/OneSteel problem rather than an operational failure, after Golding was left owed about $113.3m and NRW ultimately booked a -$110.5m impairment once its security position over Whyalla Ports came under threat.

Service Stream: Value-to-Quality Pivot

Service Stream ((SSM)) demonstrates the potential for re-rating via cash conversion. H1 FY26 reported 148.4% EBITDA-to-OCFBIT conversion, with a 80% O&M recurring revenue profile.

Expansion into Defence Base Services adds high-barrier, long-duration contracts.

Sustained execution improvement positions Service Stream to transition from a value-oriented stock to a quality-focused premium.

Cash Conversion and Valuation: Mathematical Insight

The market’s premium can be expressed via a simplified EV model:

?

Where:

- g = sustainable growth rate

- WACC = weighted average cost of capital

- Cash Conversion = probability-weighted efficiency of the work-to-cash cycle

When companies like Monadelphous and SRG convert more of their earnings into cash, their value goes up; but it is not just about the math.

Investors also see less risk, which effectively lowers the cost of capital.

That combination is why Monadelphous can trade at an 18.7x multiple, while a competitor with weaker cash conversion might sit at 8x.

The “Execution Premium” is simply the market paying for that reliability.

Table 2: Reconciling Cash Conversion Definitions (H1 FY26 vs FY25)

Lessons from Failure: Execution Capacity Defines Whether Backlog Has Economic Value

Clough Group remains the clearest recent domestic example of backlog failing to protect enterprise value.

At the point of collapse, awarded work remained substantial.

The failure emerged because project delivery costs, labour availability, fixed-price exposure, and claims pressure overwhelmed the company’s ability to convert contracted revenue into cash.

The lesson is straightforward: Backlog supports valuation only where execution capacity is credible.

Key takeaways:

- Labour Control as a Strategic Asset – direct-hire models insulate firms from cost inflation and schedule slippage.

- Annuity Re-Rating – recurring O&M work stabilizes cash flows and lifts multiples.

- Portfolio Simplification Works – focusing on core, high-quality operations increases valuation.

The Takeaway

The sector is being priced differently than it was a few years ago.

Winning work still matters, but the bigger question is whether that work can be delivered cleanly and turned into cash without disruption.

In a labour-constrained market, this is why the same contractors continue to attract premium valuations.

The market is paying less for growth alone and more for confidence in execution.

Technical limitations

If you are reading this story through a third party distribution channel and you cannot see tables included, we apologise, but technical limitations are to blame.

Find out why FNArena subscribers like the service so much: “Your Feedback (Thank You)” – Warning this story contains unashamedly positive feedback on the service provided.

FNArena is proud about its track record and past achievements: Ten Years On

Click to view our Glossary of Financial Terms

CHARTS

For more info SHARE ANALYSIS: CRN - CORONADO GLOBAL RESOURCES INC

For more info SHARE ANALYSIS: DOW - DOWNER EDI LIMITED

For more info SHARE ANALYSIS: MND - MONADELPHOUS GROUP LIMITED

For more info SHARE ANALYSIS: NWH - NRW HOLDINGS LIMITED

For more info SHARE ANALYSIS: SRG - SRG GLOBAL LIMITED

For more info SHARE ANALYSIS: SSM - SERVICE STREAM LIMITED

For more info SHARE ANALYSIS: VNT - VENTIA SERVICES GROUP LIMITED