Treasure Chest | Oct 10 2013

This story features WESTPAC BANKING CORPORATION, and other companies.

For more info SHARE ANALYSIS: WBC

The company is included in ASX20, ASX50, ASX100, ASX200, ASX300 and ALL-ORDS

By Greg Peel

“Sector Fully Valued” said JP Morgan last week. “Still gas in the tank” said Citi yesterday. For some time now, and particularly in the last twelve to eighteen months or so, the question of whether or not Australian banks are overvalued with respect to their relatively subdued earnings potential has become a common one.

For a while there, bank analysts began to concede that the global search for yield meant high-yielding Australian banks, which on a global comparison are among the least risky in the world, should be afforded a greater valuation multiple (PE) than history would suggest. A low interest rate environment ensured such leeway. Yet by September, when Wall Street was marking new highs and the ASX 200 had rediscovered 5300, even the dividend yield story was looking stretched. The earnings forecast picture just did not justify such valuations.

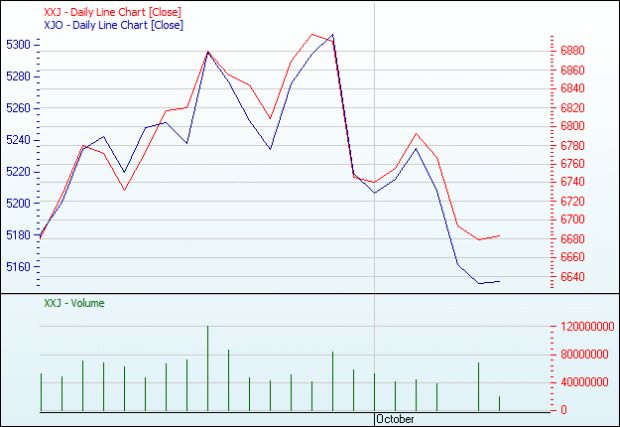

We have since had a US shutdown-related pullback, but as the following graph displays, the Australian bank sector has still outperformed. The graph shows the one month relative performance of the S&P/ASX 200 Financials ex-REITs (XXJ) as the red line and the S&P/ASX 200 (XJO) as the blue line:

Source:ASX

“Major banks are fully valued heading into the FY13 reporting season at the end of the month,” suggests JP Morgan, “and are once again trading at the top end of…their long-run trading range”.

As the analysts note, the May-June correction experienced by the ASX 200 – driven by the Fed tapering debate – did indeed see the banking sector underperform (down 15% compared to the index down 7%) but the banks have continued to grind back ever since. JP Morgan is nevertheless unusual in its stock ratings system in that it rates stocks not against the index, but within the sector that stock belongs to. Hence the broker trades off recommendations in terms of like for like.

Thus JP Morgan has preferred Westpac ((WBC)) to Commonwealth Bank ((CBA)) between the “mortgage banks”, National Bank ((NAB)) to ANZ Bank ((ANZ)) between the offshore-exposed banks and Bank of Queensland ((BOQ)) to Bendigo & Adelaide Bank ((BEN)) between the regionals. The WBC-CBA preference represents valuation versus dividend timing, the NAB-ANZ preference represents NAB’s recovery in the UK versus ANZ’s falling institutional margins, and the BOQ-BEN preference represents a credit rating increase for BOQ versus a weak FY13 result from BEN.

JP Morgan now believes those valuation gaps have closed, in light of the general outperformance of the banking sector. Ironically however, while the broker suggests the major banks are “fully valued” it has not downgraded any ratings. In fact, it has upgraded CBA to Neutral from Underweight (Westpac is Overweight), retained a Neutral on NAB and Underweight on ANZ, and upgraded Bendelaide to Neutral from Underweight (BOQ is Neutral).

By contrast, Citi maintains a Buy (equates to Overweight) on all the four majors bar NAB (Neutral).

Citi has held a strong Buy call on the banking sector for six quarters now, and continues to believe material risks to that call remain minimal. The more material risks that have threatened over that time, including regulatory capital creep, stretched valuation, excessive deleveraging, asset deterioration and margin contraction, have not become either more worrisome or more probable. On that basis, there is no indication dividend sustainability cannot remain robust, says Citi, versus both bonds and term deposits, nor yields supportive of price.

As we entered 2013, and bearing in mind bank share price had been running hard since mid-2012, the issue was one of earnings growth. In a subdued credit environment, where was the “E” going to come from to justify the already run-ahead “P” in PE ratios? But Citi notes credit growth is slowly strengthening. Since upgrading credit growth expectations in July, the broker notes new lending commitments continue to rise.

And we are still a long way from anything that might be considered overblown or dangerous on the credit growth front, the analysts point out. Furthermore, “bubble” talk in Australian property is misguided when one considers the average house-price-to-income ratio is below peak and unchanged in recent years.

As far as the risk of falling margins is concerned, lower term deposit rates and falling wholesale funding costs have killed off that argument.

Citi refers to the Australian banking sector as a “stable oligopoly”, but please don’t tell the politicians. This stable oligopoly is the key driver of superior business asset quality, the analysts suggest. The broker’s Business Stress Index has proven an accurate 2-3 year leading indicator of rising bad debts for the past four loan downturns of 2008, 2001, 1998 and 1991 but currently remains at very low levels.

So there we have it. Of two FNArena database brokers, JP Morgan says the banks are fully valued, but has upgraded the ratings on two of them, and Citi says there’s more upside potential left. The database itself shows a breakdown of fifteen Buy (or equivalent) ratings for the four majors, ten Holds and seven Sells. Even if we discount a broker’s natural tendency to encourage clients to Buy rather than Sell (and JP Morgan’s relativities), we still find an upside-biased net assessment.

Technical limitations

If you are reading this story through a third party distribution channel and you cannot see charts included, we apologise, but technical limitations are to blame.

Find out why FNArena subscribers like the service so much: "Your Feedback (Thank You)" – Warning this story contains unashamedly positive feedback on the service provided.

Click to view our Glossary of Financial Terms

CHARTS

For more info SHARE ANALYSIS: ANZ - ANZ GROUP HOLDINGS LIMITED

For more info SHARE ANALYSIS: BEN - BENDIGO & ADELAIDE BANK LIMITED

For more info SHARE ANALYSIS: BOQ - BANK OF QUEENSLAND LIMITED

For more info SHARE ANALYSIS: CBA - COMMONWEALTH BANK OF AUSTRALIA

For more info SHARE ANALYSIS: NAB - NATIONAL AUSTRALIA BANK LIMITED

For more info SHARE ANALYSIS: WBC - WESTPAC BANKING CORPORATION